Executive Summary

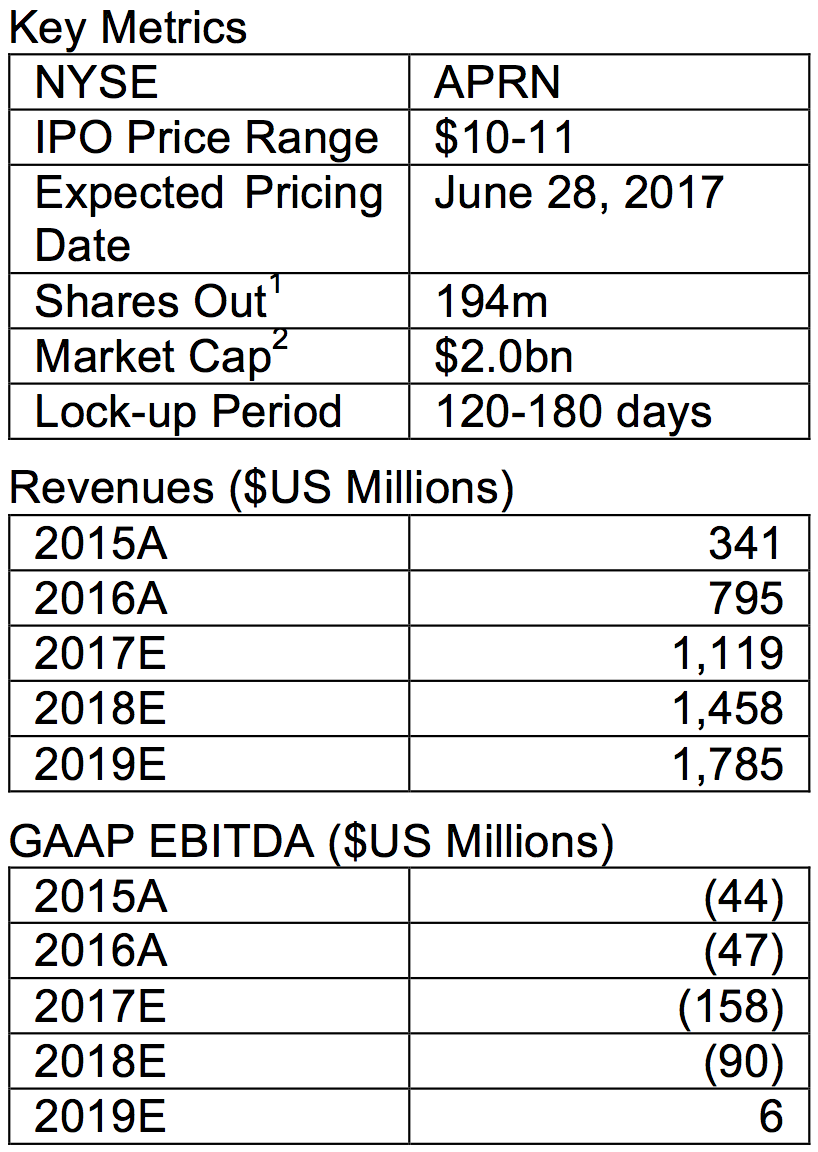

Blue Apron is a compelling first-mover and category leader that is well-positioned to scale rapidly in the $782 billion US grocery market and $540 billion US restaurant market. Blue Apron’s impressive customer and order growth, strong brand, and value-chain infrastructure enabled the company to grow revenues 133% from 2015 to 2016. However, revenue growth has decelerated to 42% year-over-year in the most recent quarter, the company will likely remain unprofitable for many years to come, and there appears to be considerable existing and future competition. The company’s IPO pricing range of $10-11 per share gives the company a market capitalization value between $1.9-2.1 billion, representing a 1.5-1.6x 2017 forward sales multiple (similar to Grubhub, Hello Fresh, and eBay sales multiples). Although Blue Apron’s valuation might not seem stretched from a multiple perspective, the company’s total market valuation relative to Whole Food’s purchase price of $13.7bn presents an interesting investment discussion given the current scale, competition, and future financial expectations.

E-commerce Eating

Founded in 2012, Blue Apron is a “cooking experience” company inspired by founders who wanted to cook at home but found grocery shopping and menu planning burdensome, time consuming, and expensive.4 They would like to make home cooking accessible to everyone and reinvent the grocery supply chain. With headquarters located in New York and fulfillment centers in California, New Jersey, and Texas, Blue Apron delivers high-quality, pre-portioned ingredients along with original recipes and content to consumers.

The Opportunity

With over 1 million paying customers ordering nearly $800 million in revenues in 2016, Blue Apron is a compelling first-mover and category leader that is well-positioned to scale rapidly and take market share in the $782 billion US grocery market and $540 billion US restaurant market.5 Of this $782 billion US grocery market, only 1.2% is online.6 Additionally, the company’s vertical integration, data analytics, and strong brand will help them compete against existing players and new entrants. US meal plan delivery accounted for approximately $2.0 billion of sales in 20167, which implies Blue Apron had 40% market share. Therefore, the company has a strong start to capturing a large opportunity as grocery stores and restaurants move more of their business online and/or via delivery.

The Risks

One of the biggest risks to any business is competition, and with Amazon’s recent acquisition announcement of Whole Foods, Blue Apron will have to compete against one of the most disruptive companies today in addition to the other start-up companies in the meal-kit/delivery category. A key advantage for Blue Apron is its brand, and the company is investing in marketing (both online and offline) to acquire new customers and fend off the competition. This might prove to be a good strategy given other start-up companies might not have the capital to keep up with Blue Apron. However, the risk to this strategy and to the viability of the business is that the company is cash flow negative and will likely remain cash flow negative for the next several years unless there is an acceleration in revenues or significant margin improvement.

Highlights:

- Blue Apron is a category leader and has a reasonable valuation relative to market comparable companies (especially given its sales growth rate) at a 2.3x 2017 EV/S multiple. However, one could argue that this valuation is close to one-fourth the purchase price of Whole Foods Market and hence not reasonable or cheap.

- 159 million meals delivered to households across the US, which represents approximately 25 million paid orders.

- Over 300 food suppliers with approximately 70% of food spend with exclusive suppliers.8

- Amazon’s acquisition of Whole Foods may be a net positive for the industry and catalyst for consolidation. Blue Apron may be a benefactor given its 1) attractive customer base, 2) brand strength, 3) category leadership, and 4) vertical integration (which is unique in the sector).

Potential Concerns:

- Significant competition, especially from a combination of Amazon and Whole Foods Market.

- Slowing growth in customers and orders, especially in the most recent quarter.

- High customer churn, which might require high levels of marketing and incentive/promotion expenses.

- Company had negative $86 million in 2016 free cash flow9 and may not be cash flow positive for many more years, especially with increasing marketing expense.

Market Landscape

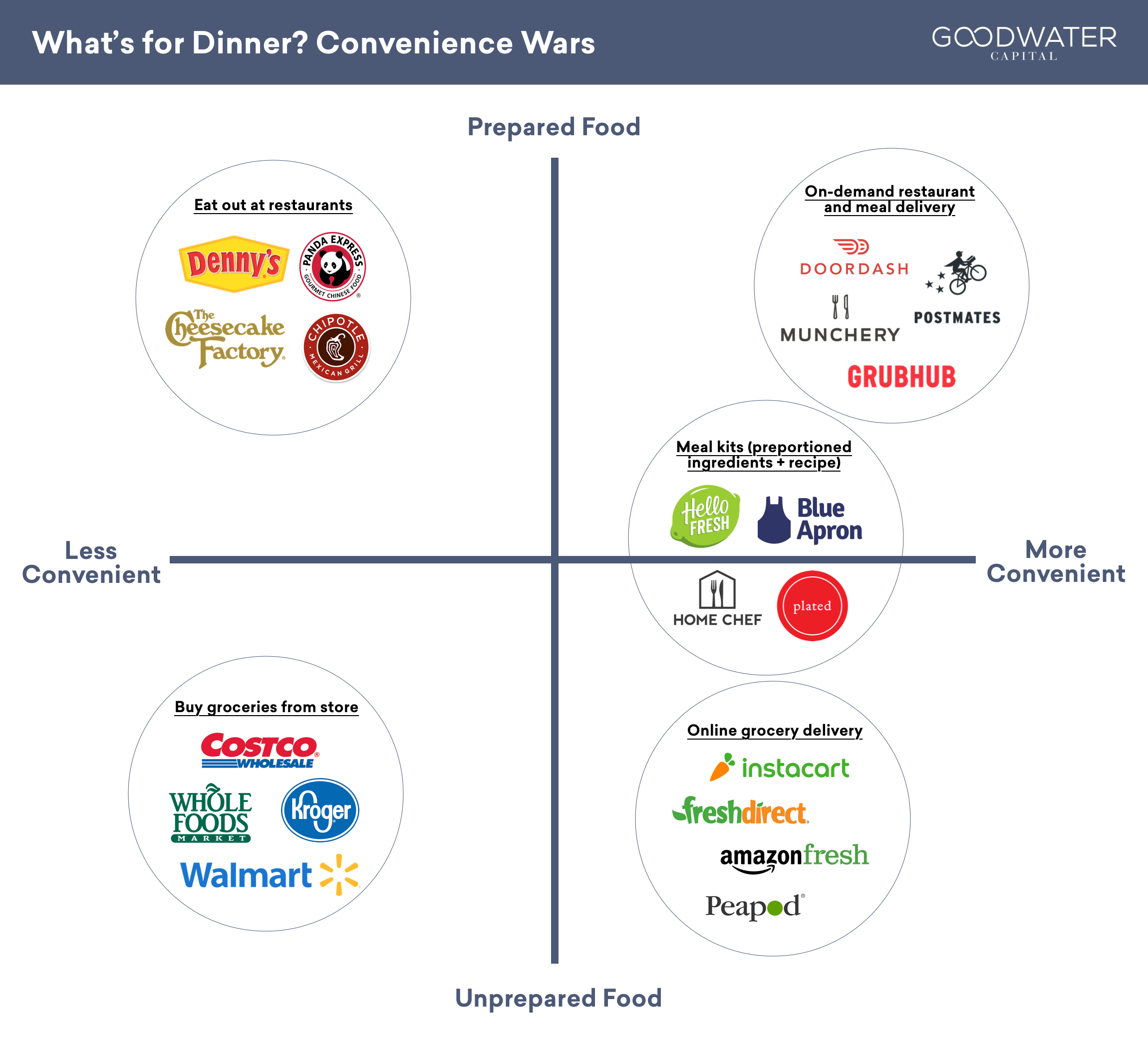

Blue Apron competes with a number of incumbent and new companies in the food category, which is a highly competitive space with challenging margins, plentiful alternative options, and high marketing spend. The opportunity could be significant if this market transitions online. However, it is very early in this transition and the future leaders in this category are still to be determined.

Meal planning and cooking are considered chores by many, and consumers are placing an increased value on the ability to save time and effort. Largely an offline behavior today, food and grocery delivery as a market will increasingly leverage technology, transitioning users to online and mobile and offering increased convenience and efficiency. The on-demand economy combined with the large grocery and food market present a great opportunity for companies to offer consumers new services with various levels of effort to create meals and convenience (time or distance from consumer).

- On-demand restaurant and meal delivery services provide a centralized platform for ordering and delivering meals from a variety of restaurants. Consumers order food from an online platform and can receive a hot restaurant meal within an hour. Startups Postmates and DoorDash have a strong market presence, alongside larger companies such as GrubHub Seamless, Square’s Caviar, Yelp’s Eat24, and Uber’s UberEats. Meal delivery services deliver complete meals that are often designed and prepared by professional cooks and are fresh and ready to consume within minutes. Menu choices are generally limited, and offer quick healthy options for those who do not want to cook. With the recent shut down of Maple and Sprig, Munchery and Freshly are leaders in this space.

- Meal kits are services that send boxes of pre-portioned ingredients to consumers, who then prepare home-cooked meals following a step-by-step recipe included in the box. Plated and HelloFresh are two of Blue Apron’s biggest competitors. Within the category, there is a multitude of specialized offerings such as Sun Basket (organic, paleo, and gluten free), Home Chef (personalized based on inputted meal preferences), Purple Carrot (vegan), and Gobble (10 minutes with 1 pan).

- Online grocery delivery offers ordering options and fast delivery for all types of grocery products. Services vary with respect to geographic coverage, fees, and selection. Examples include Instacart, FreshDirect, Amazon Fresh, and Peapod, as well as specialized grocery delivery services like Good Eggs and Thrive Market that focus on organic products.

- Traditional offline grocers like Costco and Walmart and restaurants ranging from fast food to full-service experiences are overwhelmingly the incumbents in the food and grocery space. Large retail grocers have several potential advantages, including existing robust infrastructure and supply chains, a large base of relevant customer data, and the ability to stock their own meal kits.

Competition and Amazon/Whole Foods Market – Elephant in the Room

It is too early to determine the impact that this combination will have on the overall food services sector, but companies that fall within food logistics will be the most negatively impacted in the near-term due to the operational and fulfillment scale of an Amazon and Whole Foods combination. No matter the success or failure of this acquisition, the $1.3 trillion US grocery/restaurant sector is ripe for continued disruption, and the transition from offline to online retailing only has single-digit penetration today.

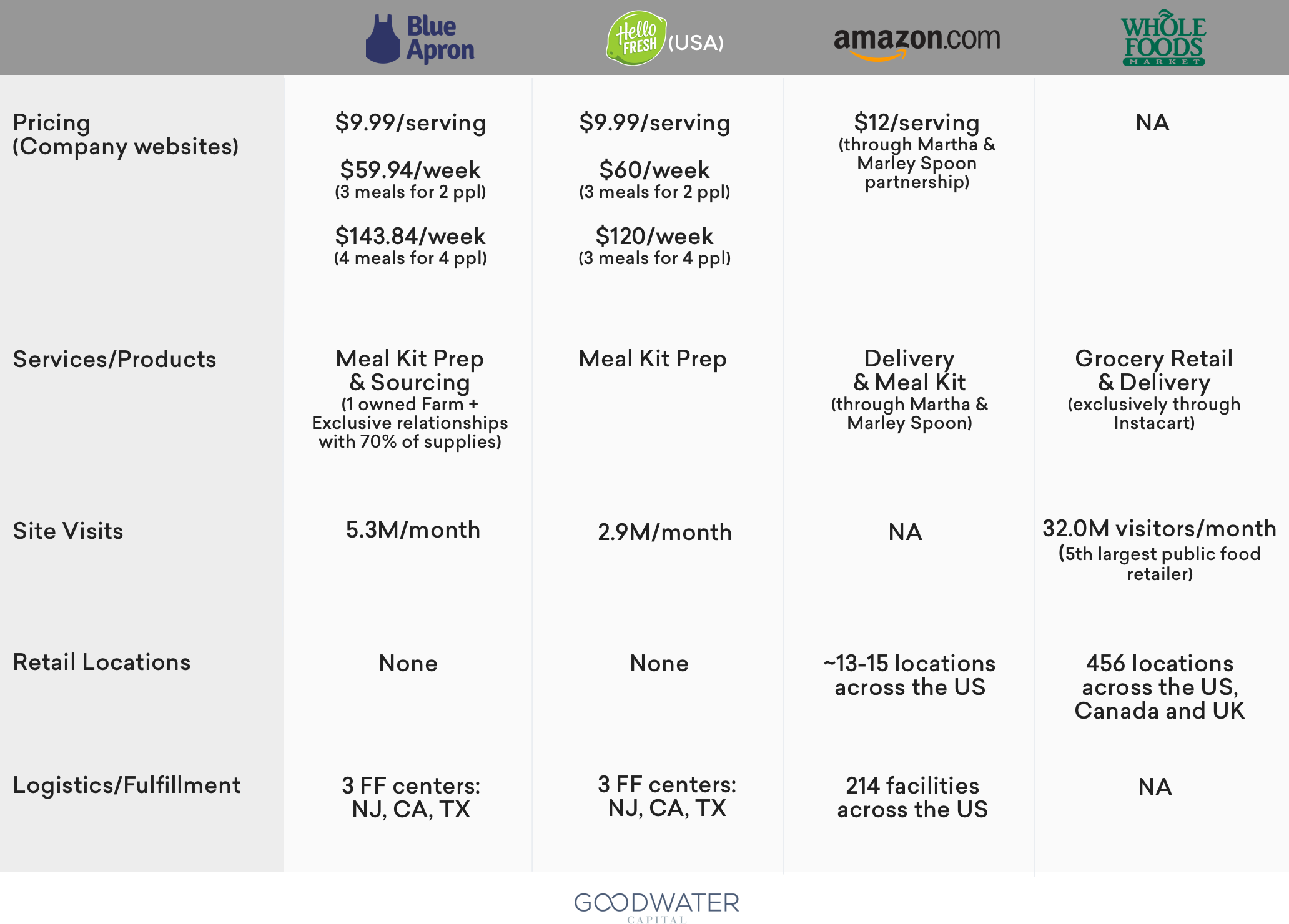

Blue Apron’s innovative home-kits represent a new way to address the “last mile” problem that so many service providers struggle to overcome in terms of both convenience and price. While Blue Apron generates nearly two times the revenue of its closest competitor (i.e. HelloFresh US), both leaders in the meal kit delivery space are dwarfed by the revenues generated by Whole Foods alone at $15.7B.

However, revenue growth of these two players (133% and 176% for Blue Apron and HelloFresh USA, respectively) was much faster than that of Whole Foods with only low single-digit growth over the last few years. Blue Apron’s gross margin of 33% is in line with both Amazon and Whole Foods, reflecting some of the benefits that it has achieved through its supply chain and fulfillment network, and is nearly 3x the gross margin of HelloFresh USA.

Given the competition in the market, both Blue Apron and HelloFresh meal plans are priced similarly at $9.99 per serving per person, with multi-person servings per week starting at approximately $60/week (three meals for two people per week). Amazon Fresh currently offers a meal kit delivery service through a partnership with Martha Stewart and Marley Spoon at $12 per serving. Blue Apron also offers complimentary products including branded wine, cutlery, and food-related media, such as published cookbooks.

However, with Amazon’s acquisition of Whole Foods, the largest and most efficient distribution system (Amazon) now has natural/organic fresh food (Whole Foods) that is relevant to Blue Apron’s core customer base of people with discretionary income and similar attributes (i.e., environmentally conscience, urban, affluent, values experiences, etc.). Operationally, Amazon’s acquisition of Whole Foods Market adds over 450 physical locations in desirable, neighborhood markets to Amazon’s hundreds of fulfillment centers, creating a formidable, extensive network of logistics and retail outlets in high-traffic, attractive locations across the US, Canada, and the UK, generating an average 32 million visitors per month.10 By comparison, Blue Apron has only three fulfillment centers (similar to HelloFresh) but has started to vertically integrate with an owned and operated farm (with ~70% of food spend with its exclusive suppliers).11

Goodwater Consumer Research

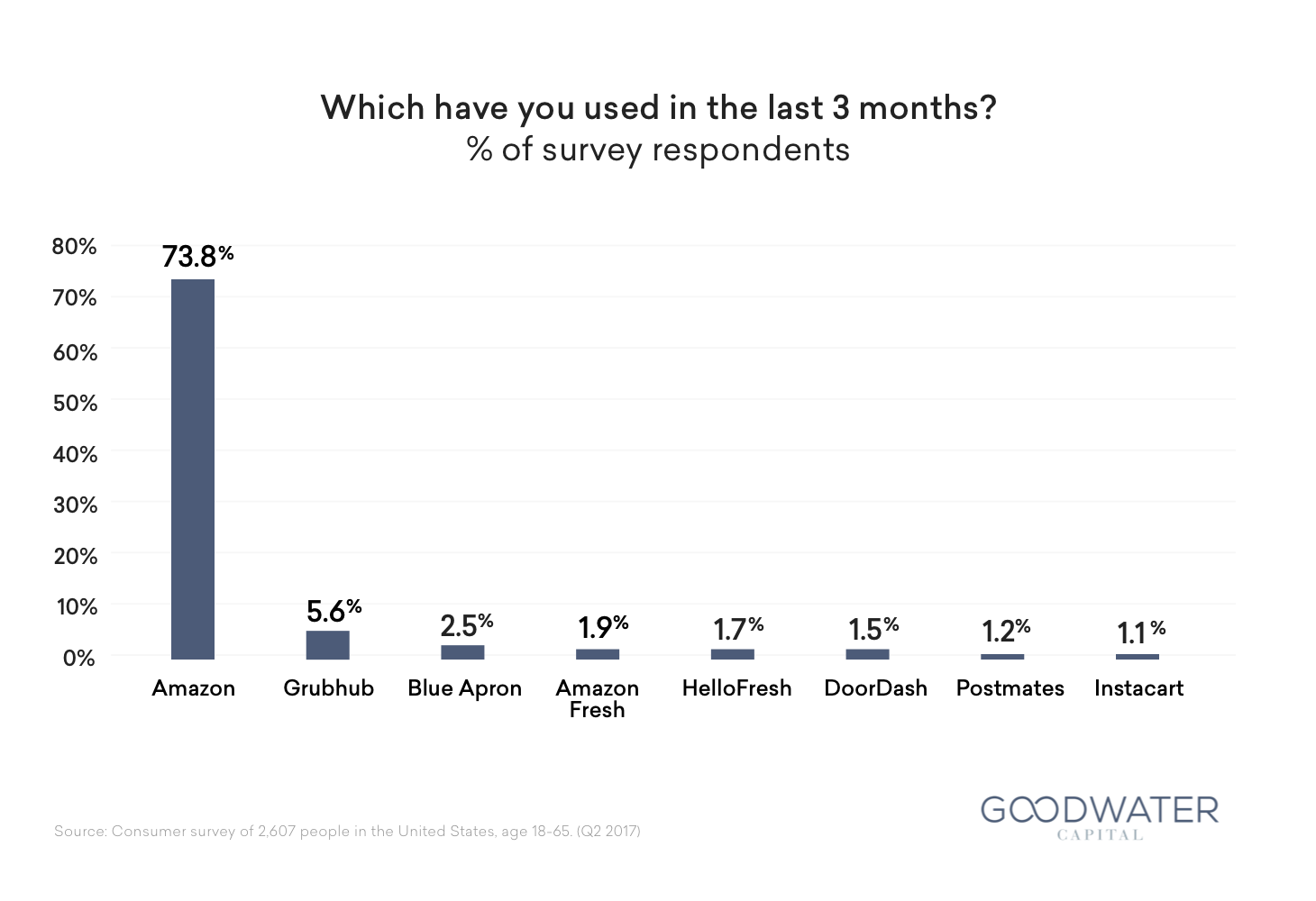

We conducted a consumer survey in June 2017 with 2,607 participants in the United States. The panel was representative of census data, balancing age, income, gender, and geography. Survey respondents reported on their usage across a broad range of consumer technology products and services, along with their sentiment and usage expectations.

We observed that food-related consumer technology services had much lower usage penetration relative to other consumer technology categories. Compared to 73.8% of survey respondents who used Amazon in the last 3 months, usage of food-related services in the last 3 months ranged from 1.1% (Instacart) to 5.6% (Grubhub). This indicates that utilizing food services facilitated by technology are is a nascent behavior, and we have yet to see whether it will achieve mass market adoption.

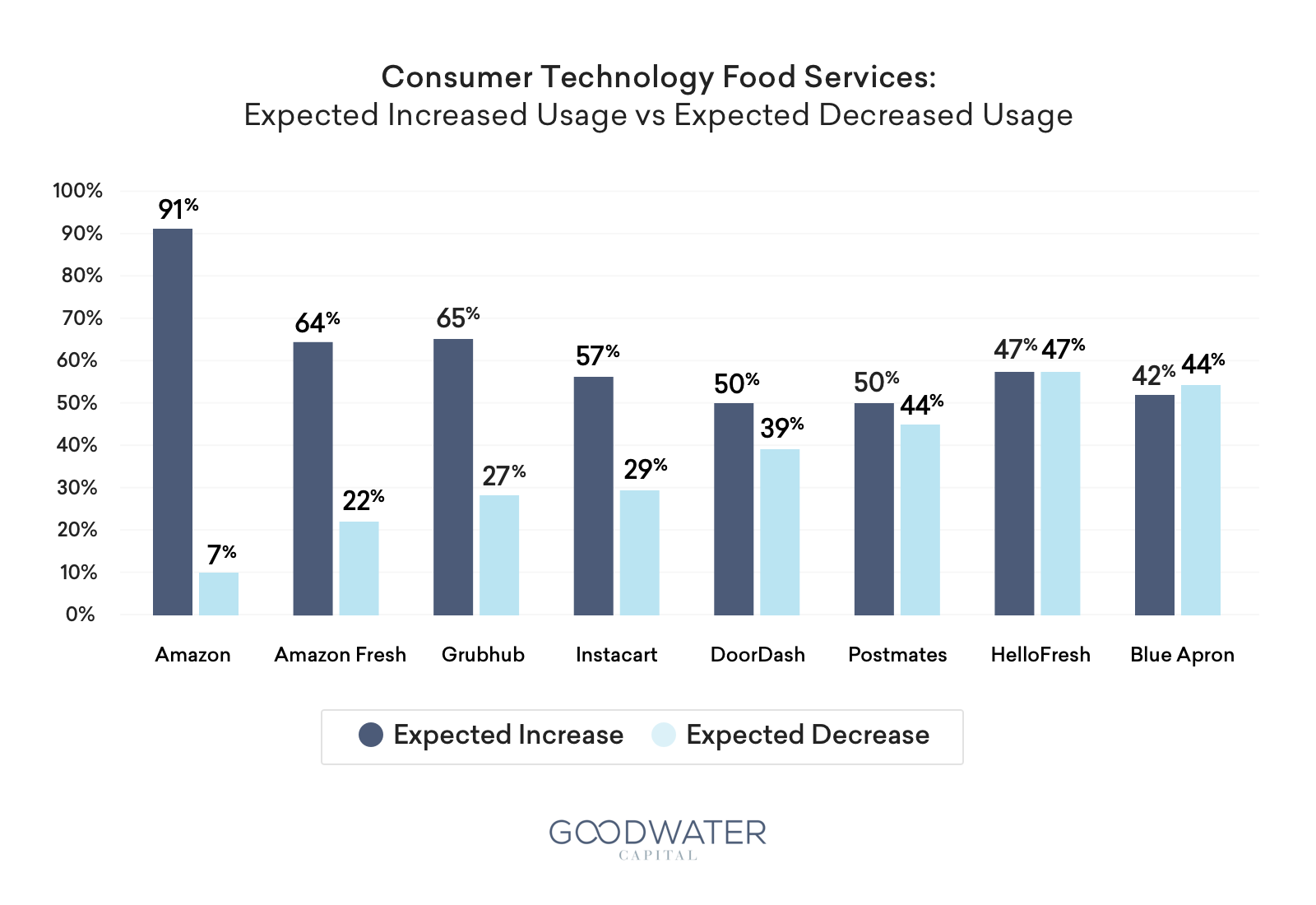

For each product or service used, survey participants also reported on which they expect to continue using or use more of, as well as which they expect to stop using or use less of. Food-related services with the highest expected usage increase were Grubhub (65%), Amazon Fresh (64%), and Instacart (57%). Conversely, services with the highest expected usage decrease were HelloFresh (47%), Blue Apron (44%), and Postmates (44%).

Comparing expected usage increase to expected usage decrease, we can infer how satisfied consumers are with the service or product. Consumers are most satisfied with Amazon Fresh, Grubhub, and Instacart; this is reflected by a high percentage of users who expect to keep using those services and a low percentage of users who expect to use them less. With 42% of users expecting to use the service more and 44% expecting to use the service less, the data for Blue Apron along with direct competitor HelloFresh indicate potential challenges with user churn, especially in the meal kit space.

Blue Apron Business Overview

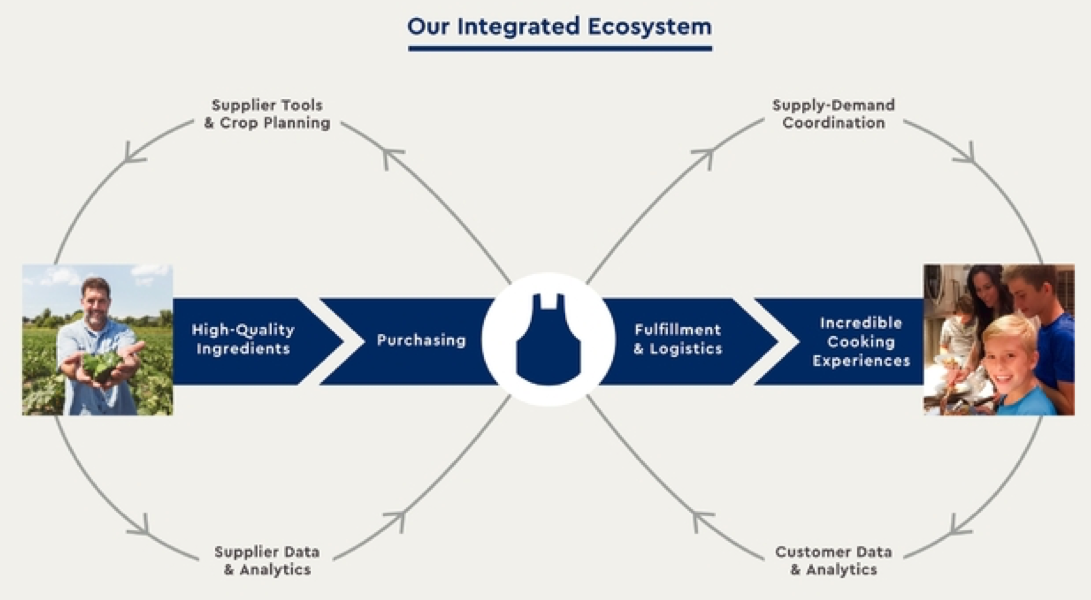

Founded in 2012, Blue Apron is a “cooking experience” company whose goal is to make home cooking accessible to everyone. With headquarters located in New York and fulfillment centers in California, New Jersey, and Texas, Blue Apron delivers high-quality, pre-portioned ingredients along with original recipes and content to consumers. The company’s vision is to build a better food system, transforming the way food is produced, distributed, and consumed via an integrated ecosystem that drives end-to-end value.

Since its inception, Blue Apron has delivered over 159 million meals to households across the United States, which represents approximately 25 million paid users. Generating almost $800 million in revenue in 2016, Blue Apron is a compelling first-mover and category leader that is well-positioned to rapidly scale and take market share in the $782 billion US grocery market and $543 billion US restaurant market.

The company makes money by offering meal plans, distributing wine directly to consumers (called Blue Apron Wine and launched in September 2015), and providing an e-commerce marketplace to buy cooking tools, utensils, and pantry items (called Blue Apron Market and launched in November 2014). The company does not break out revenues for these specific businesses, so we are assuming the newer businesses are smaller than the offering meal plans meal-kit business, and more disclosure will be given once these businesses become more significant to the overall company.

Two Meal Plan Offering12:

- 2-Person Plan includes three recipes per week (chosen from six options), each of which serves two people. This plan costs $59.94 per week, or $9.99 per person per meal (serving), and shipping is free.

- Family Plan includes two or four recipes per week (chosen from four options), each of which serves four people. For new customers, this plan costs $71.92 for two recipes per week or $143.84 for four recipes per week, or $8.99 per person per meal (serving), and shipping is free.

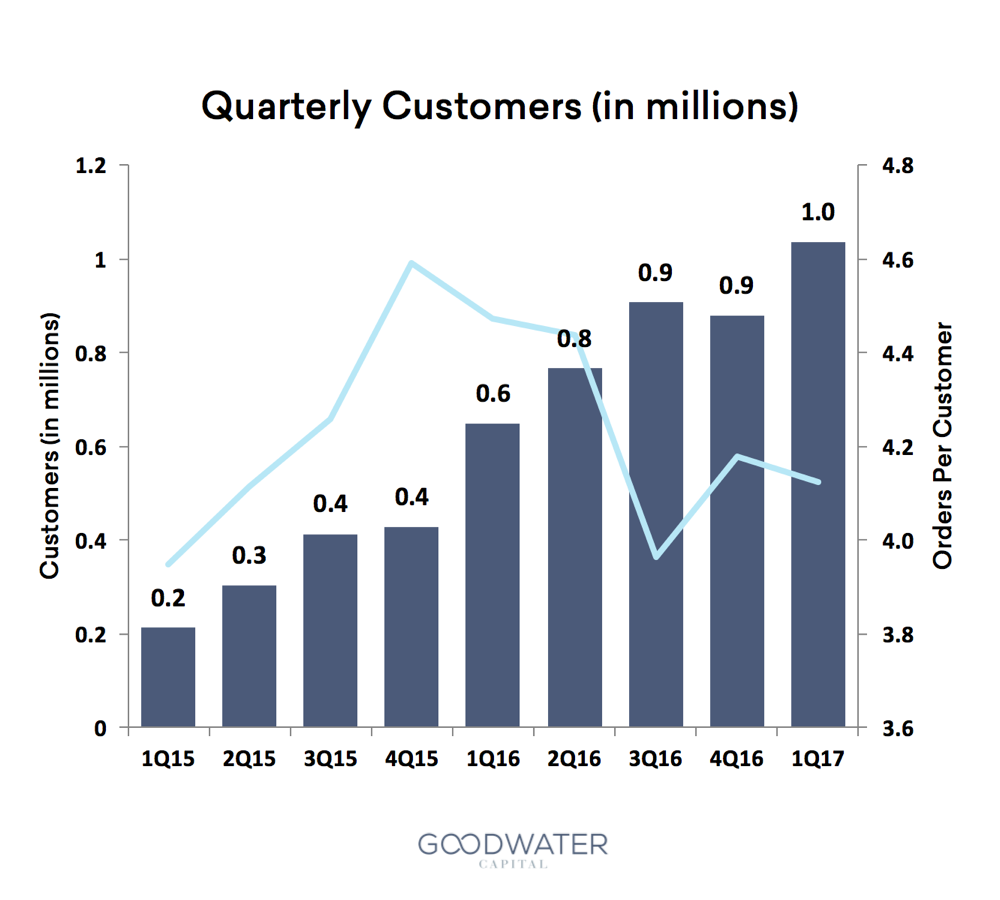

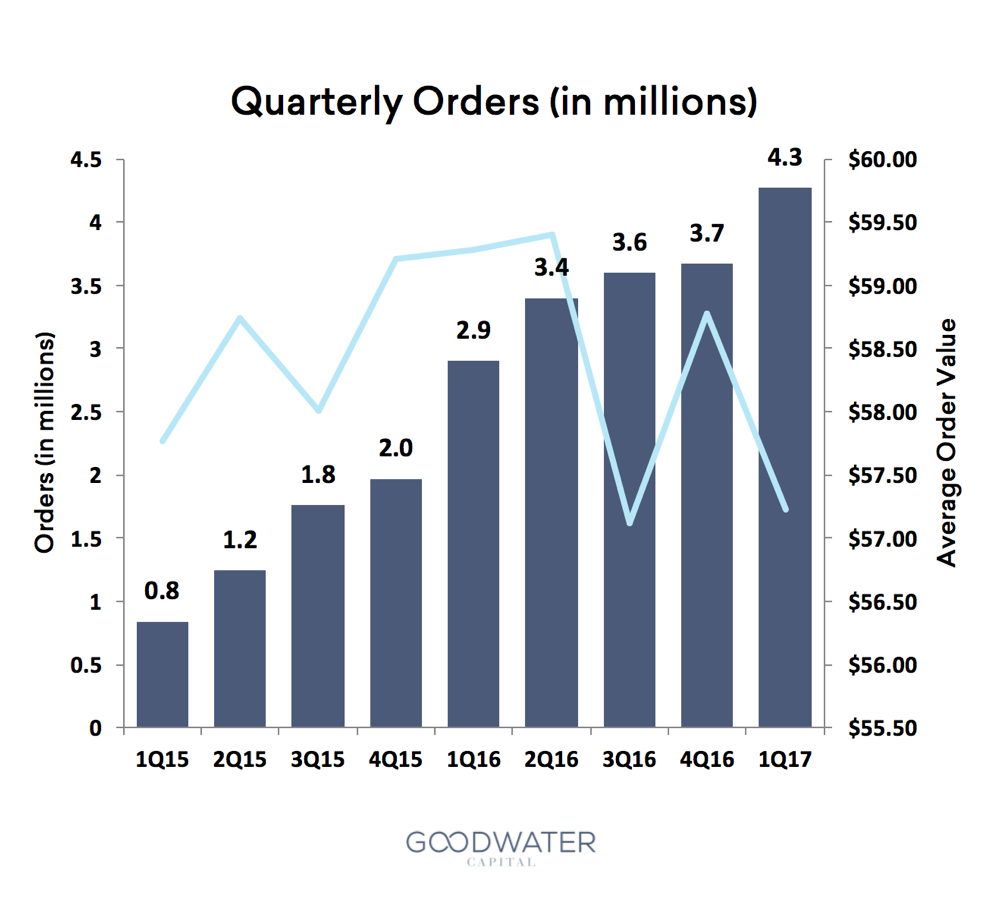

Based on the number of orders in 2016 per plan type, 78% of meal orders were for the 2-Person Plan and 22% were for the Family Plan. The average order value has been range bound ranged from $57-60 and the orders per customer has also been ranged bound from 4.0-4.6 for the last two years. Whereas, The number of customers and orders have grown significantly over the same two year period, as you can see in the below graphsillustrated in the charts below.

Blue Apron has architected an integrated ecosystem that enables them to source high-quality, differentiated ingredients, design original recipes around those ingredients, and combine them into compelling cooking experiences that they deliver to customers across the United States. Their interconnected end-to-end value chain allows them to execute cost-effectively and at scale.13 This is a unique and differentiated offering that, if successful, could make a sizable impact to in the way people buy food and eat at home.

In 2016, Blue Apron purchased from over 300 food suppliers. Approximately 70% of their food spending in 2016 was with suppliers who had entered into exclusivity arrangements with the company in which they have agreed not to supply any other company that sells boxed meals or recipes and pre-portioned ingredients to consumers. Blue Apron’s direct relationships allow them to deliver flavorful and unique ingredients in a scaled and cost-effective way.14

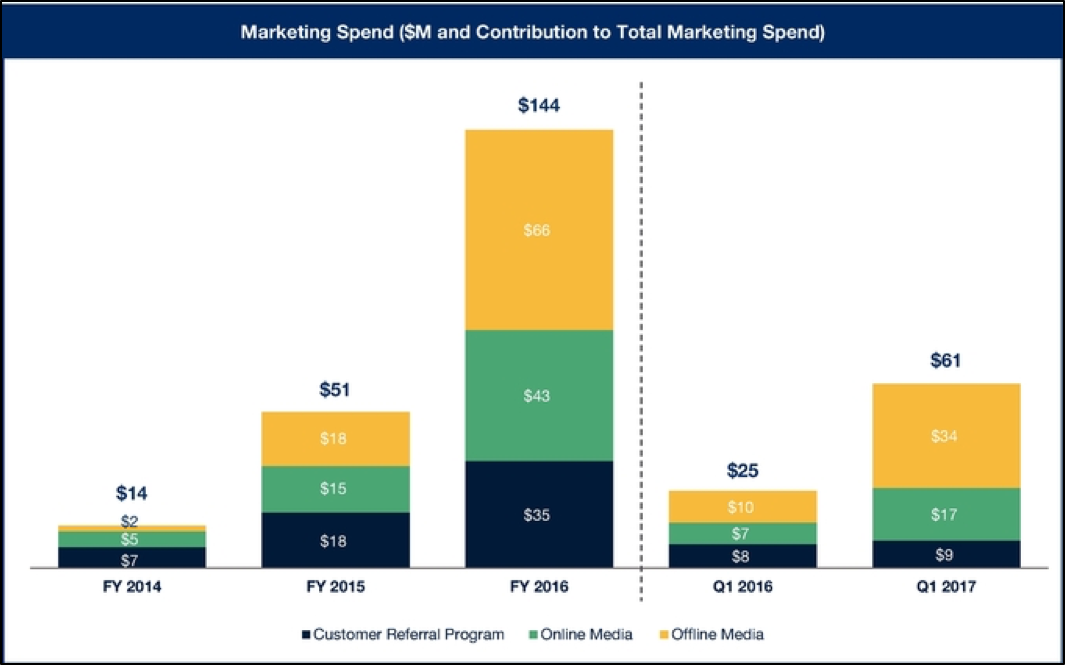

A key advantage for Blue Apron is its brand, and the company is investing in marketing (both online and offline) to build its brand, acquire new customers, and fend off the competition. This might prove to be a good strategy given other start-up companies might not have the capital to keep up with Blue Apron. However, the risk to this strategy and to the viability of the business is that the company is cash flow negative and will likely remain cash flow negative for the next several years unless there is an acceleration in revenues or significant margin improvement.

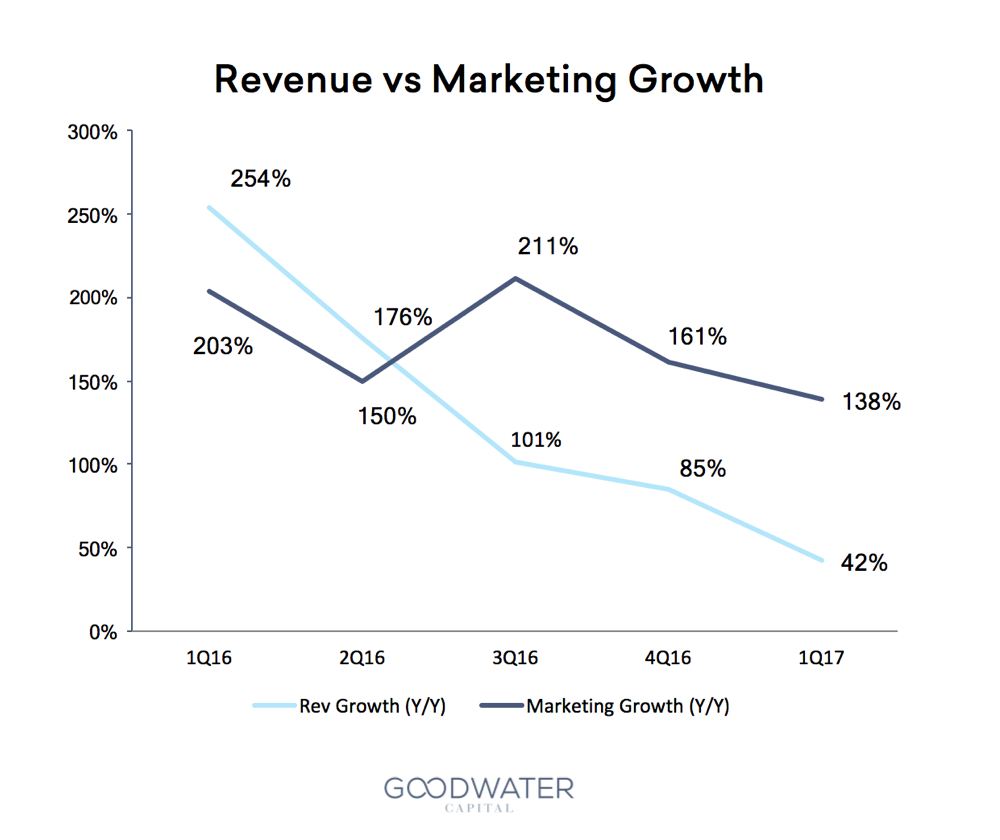

In 2016, Blue Apron’s offline media advertising spend grew 267% whereas its total marketing spend increased 181%. The significant increase in offline media advertising spend will help the company’s brand awareness but will also increase customer acquisition costs (“CAC”) in the near-term. In the most recent quarter, marketing spend increased 138% year-over-year with a 240% increase in offline media advertising spend while sales grew 42% over that same period.

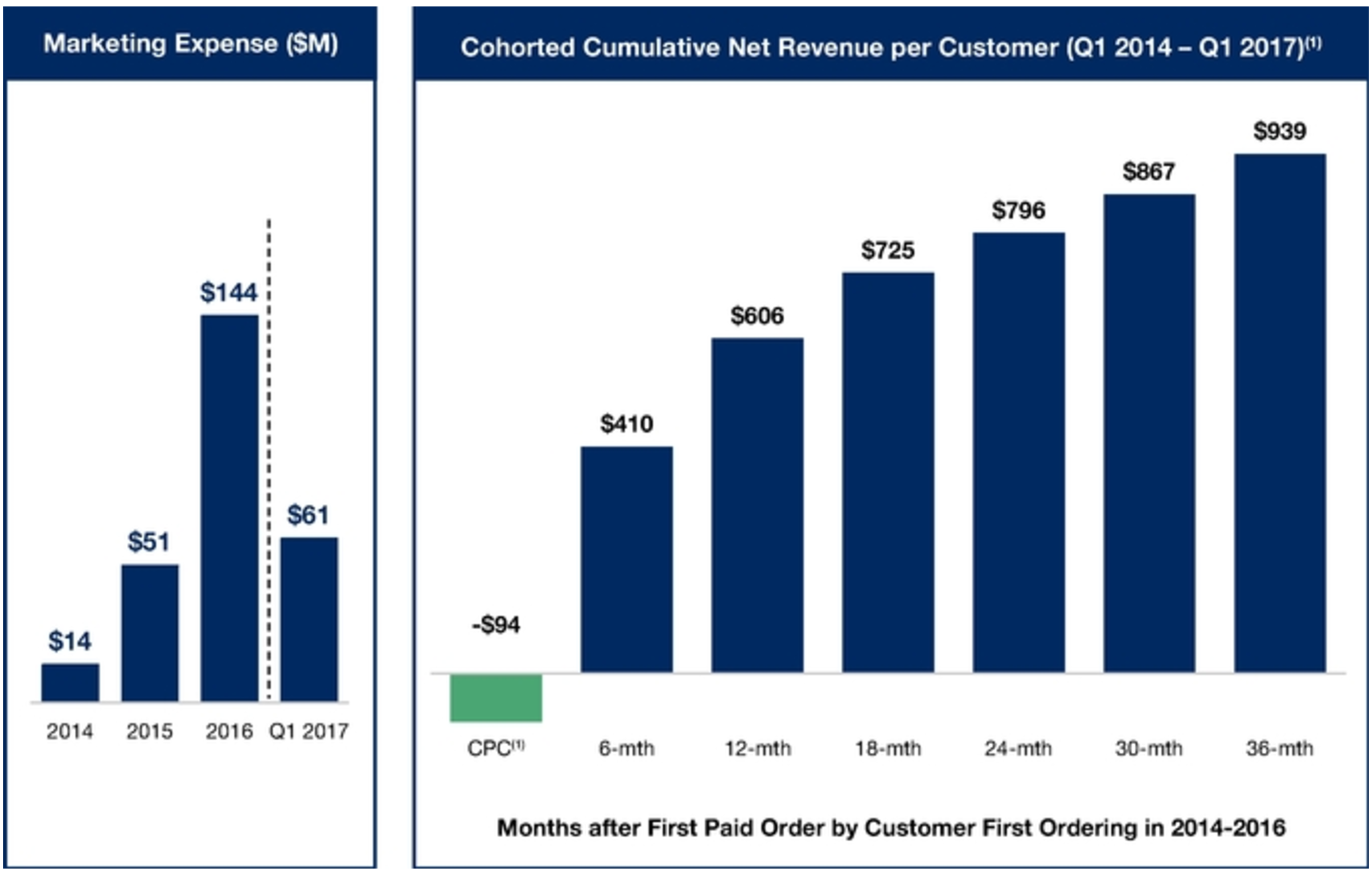

The company reported $94 CAC, which is an average from 2014 to the first quarter of 201715. However, the recent increase in marketing spend suggests current CAC should be higher than $94. The life-time value (“LTV”) of a customer is $410 for 6-months. At a 33% 2016 gross margin, the $135 LTV contribution more than pays for the $94 CAC. However, the increase in CAC will likely extend the payback period of a new customer to greater than 6 months. The company’s customer retention and LTV/CAC improvements will be critical for the timing of the company’s profitability.

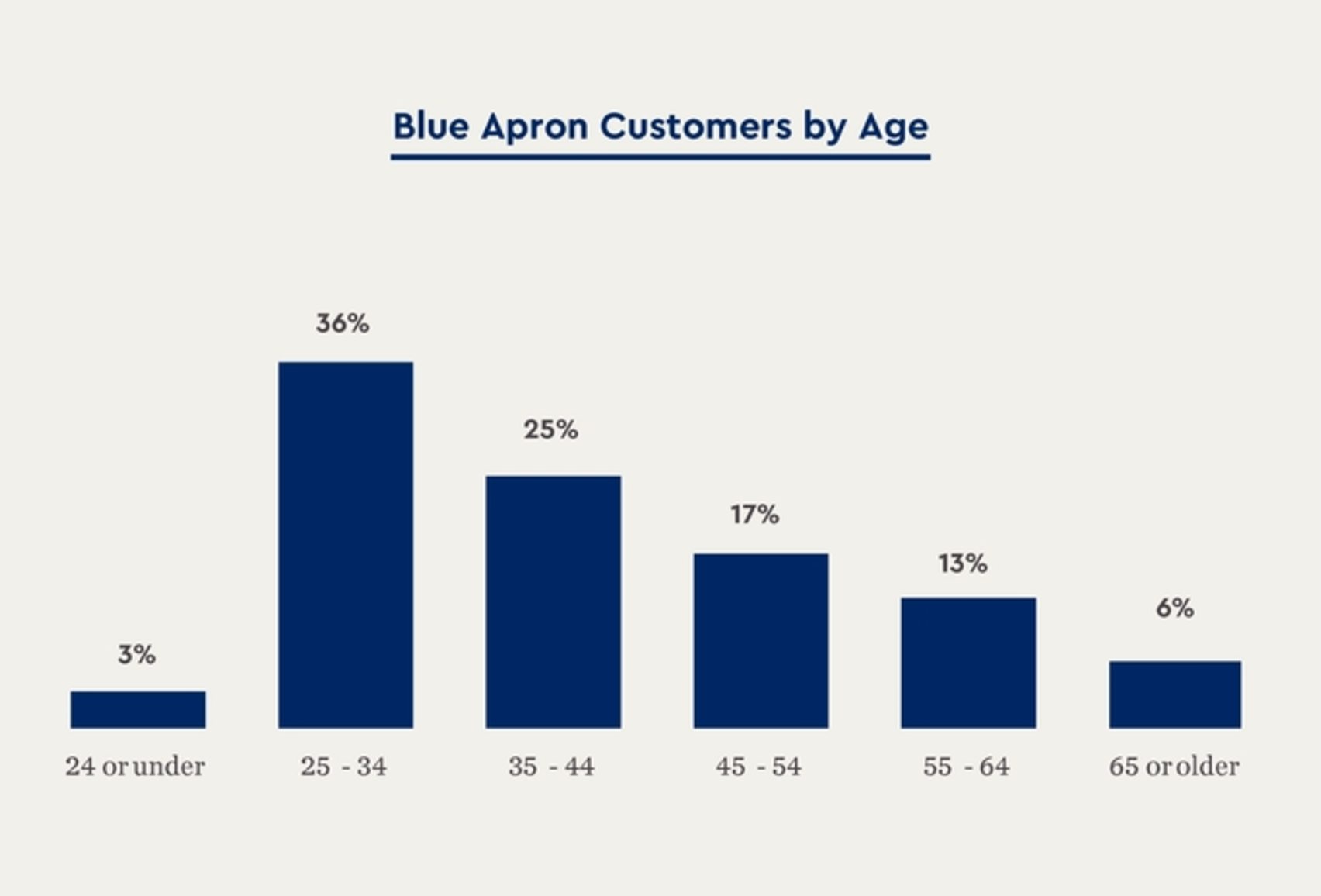

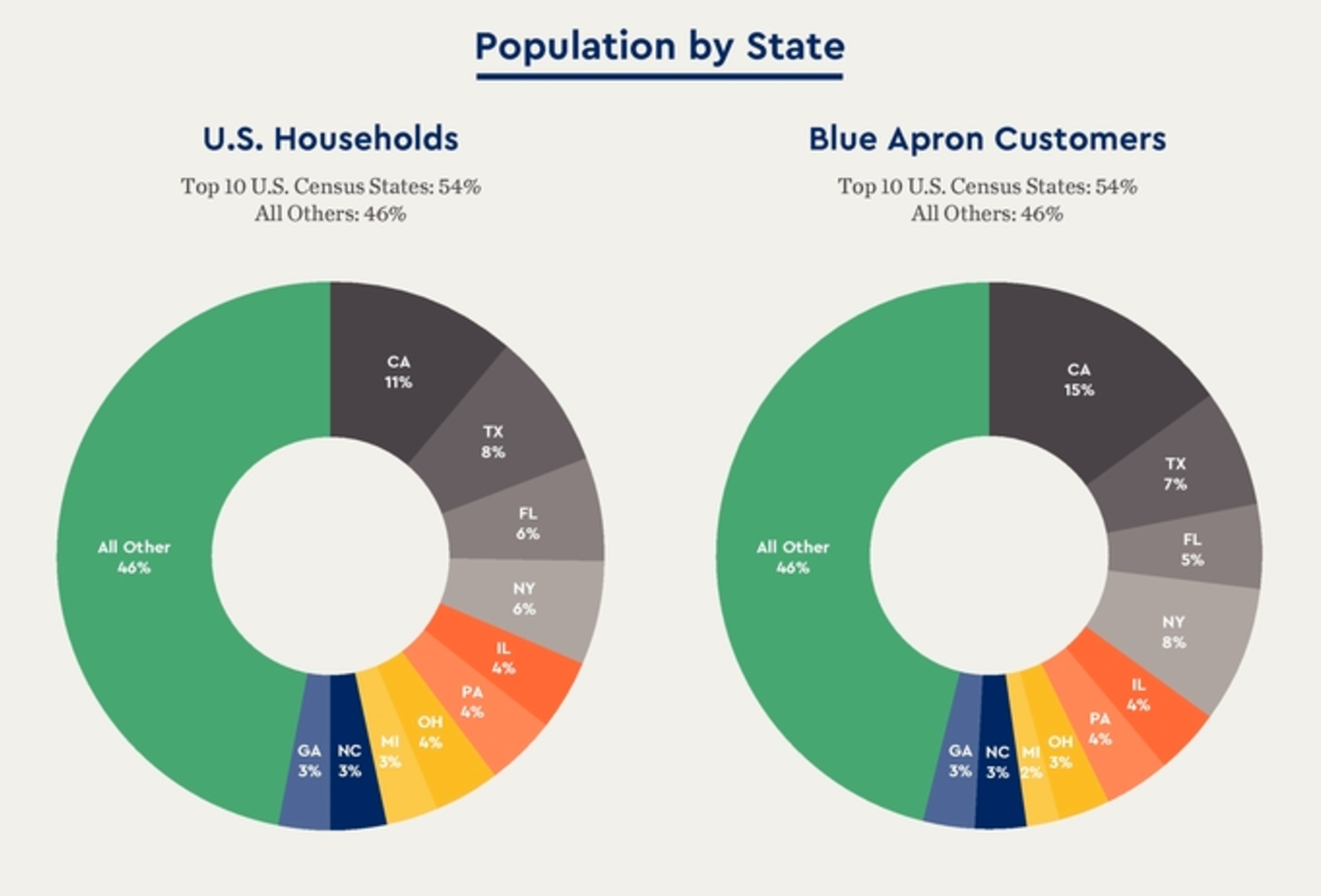

The company’s customer base is diverse both geographically and demographically. Sixty-one percent of customers are in the 25-44 age group and geographically, the distribution of customers by state closely mirrors that of the overall US population. Having established a solid customer base, Blue Apron seems to be positioned well for growth.

Key Risks

There are a number of risk factors to Blue Apron’s long-term prospects, including:

- Blue Apron’s growth and success depend heavily on customer and order growth. Unfortunately, there seems to be slowing growth in customers and orders, especially in the most recent quarter.

- High customer churn, which might require high levels of marketing and incentive/promotion expenses to offset this churn.

- Company had negative $86 million in 2016 free cash flow and may not be cash flow positive for many more years.

- The company has significant competition, especially if Amazon acquires Whole Foods Market.

- Blue Apron is a grocery and restaurant company and is exposed to the macro risks of weakening economies and lower discretionary spending.

- The company already sees seasonality in its business, which might indicate a slowing and maturing

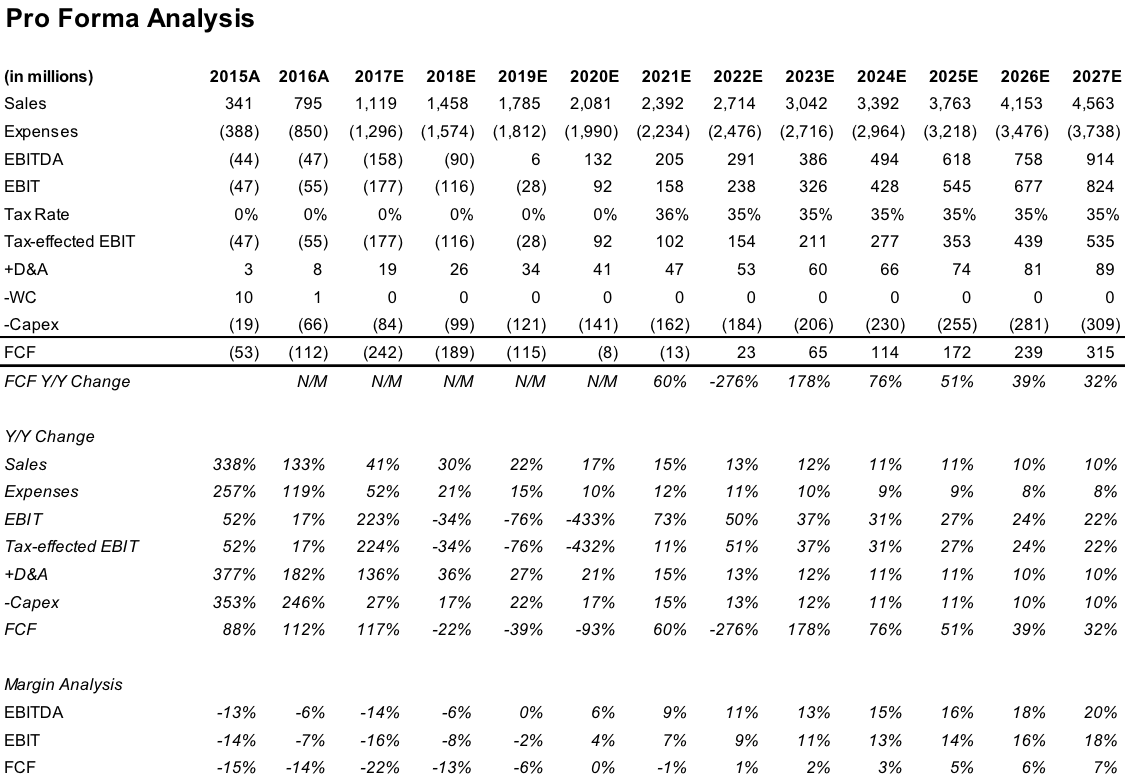

Summary Financials & Projections

Without company guidance or broker research estimates, we constructed an illustrative pro forma based on the company’s historical results and trends to calculate projected free cash flow.16 Below are a few highlights from our pro forma analysis.

- Overall gross revenue growth from $795 million in 2016 to $4.6 billion by 2027

- Free cash flow from -$112 million in 2016 to $315 million by 2027

- 20% of EBITDA margins by 2027, up from -6% EBITDA margins in 2016

- 18% operating margin by 2027

- Targeting profitability in 2019

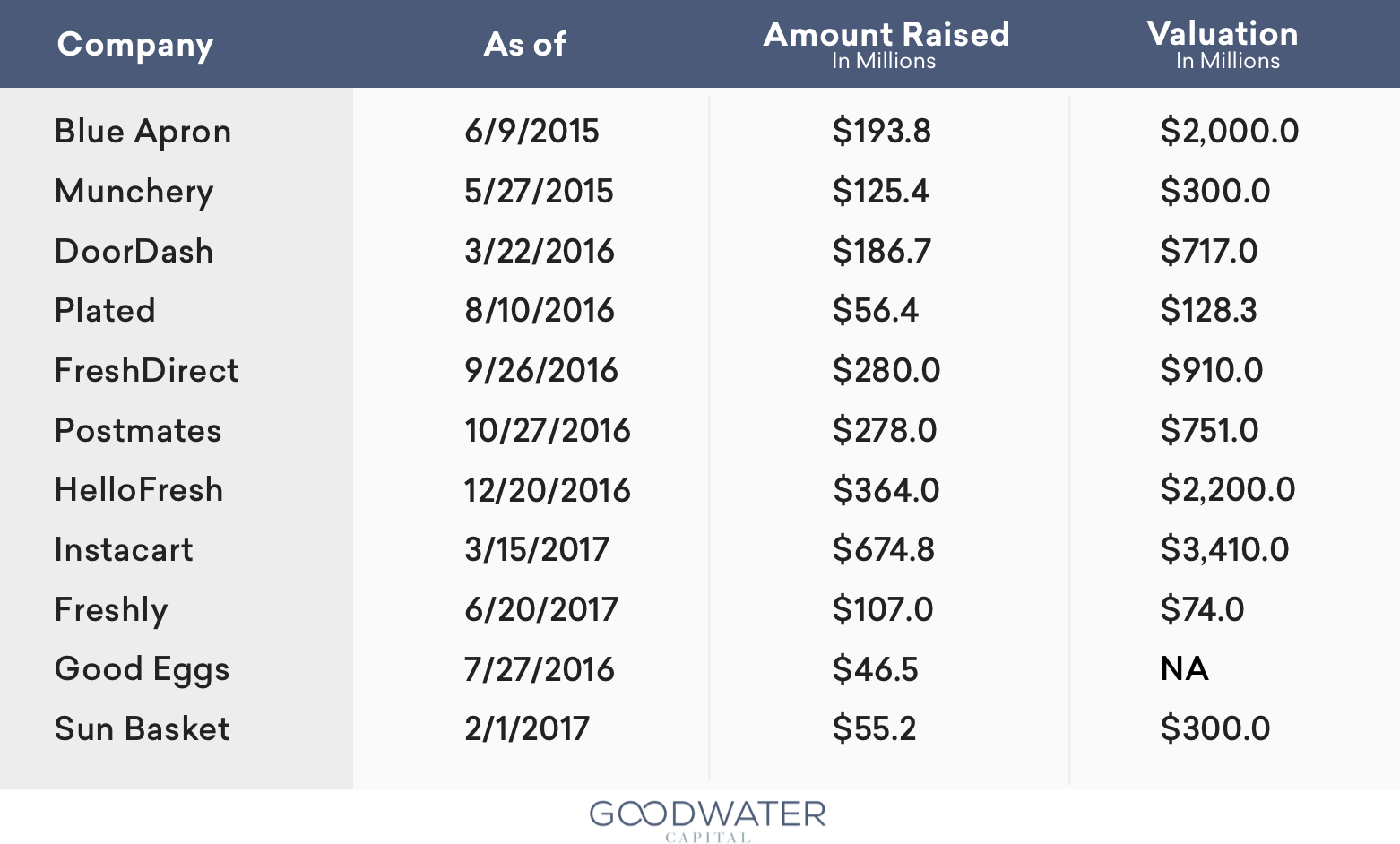

Relevant Funding and M&A

Blue Apron has raised $194 million since inception, with the last round in June 2015 valuing the business at an estimated $2 billion. Overall the US food tech sector has raised well over $2.3 billion in the last two years.17

There have been significant mergers and acquisitions in the food tech industry globally (Delivery Club, Foodpanda, RedMart, Tasty Khana, etc.). Within the US, below are the notable transactions in the sector.

- Eat24 (February 2015): acquired for $134 million by Yelp.18

- Caviar (August 2014): acquired for $44 million by Square.19

- Seamless and GrubHub merger (May 2013): Seamless representing 58% and GrubHub representing 42% of the equity of the combined business; the merger was finalized in early August 2013 for a combined value of $422 million.20

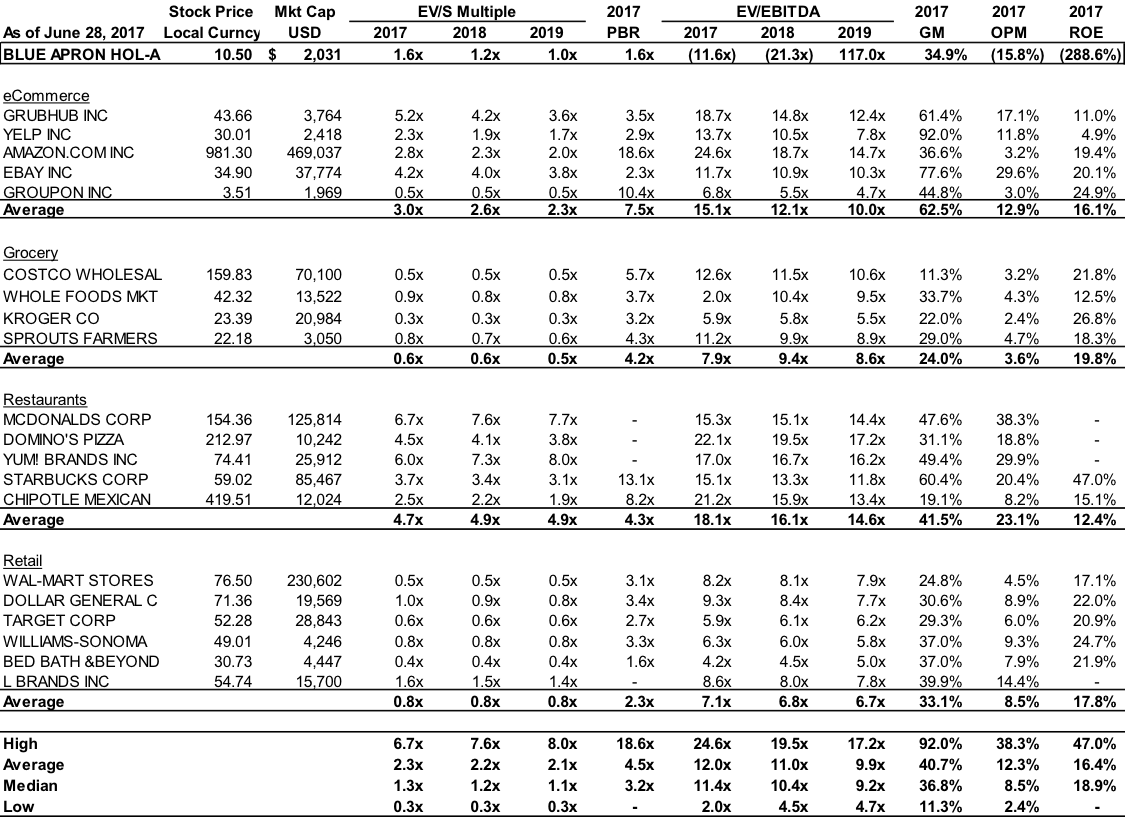

Public Comparable Companies

The above public comparables indicate that its valuation has a wide range but could trade around a 2x forward sales multiple if it trades around the average of the above comp set.

Executive Team

- Matt Salzberg (co-founder & CEO): Prior to founding Blue Apron, Matt was a venture capital investor at Bessemer, where he focused on mobile, digital-media, and software. He holds a B.A. in economics and an MBA, both from Harvard University.

- Ilia Papas (co-founder & CTO): Ilia was a director and technical architect at Optaros. He has also built solutions for RueLaLa.com, CNN, PUMA, Turner Broadcasting, and Macy’s. He holds a B.S. in computer science from Tufts University.

- Matthew Wadiak (co-founder & COO): After graduating from The Culinary Institute of America, Matthew cooked for various notable chefs, founded a catering and events company, and spent several years sourcing and importing rare ingredients for chefs and food companies around the world.

- Bradley Dickerson (CFO): Bradley was CFO and COO at Under Armour, where he helped drive the company from a pre-IPO position into a publicly traded firm with $4 billion in revenue. Previously, he was CFO at Macquarie Aviation North America and CFO at Network Building & Consulting. He holds a B.S. in accounting from University of Akron and an MBA from Loyola University Maryland.

- Jared Cluff (CMO): Jared was SVP marketing at Fab.com, COO AvidTrips, SVP marketing at Ask.com, and online marketing director at Match.com. He holds a B.A. in economics from Stanford University and an MBA from Northwestern.

- Fully diluted shares outstanding calculated using 187 million basic shares outstanding plus 7m shares in greenshoe option and treasury method for options outstanding using $10.50/share (i.e. midpoint of the $10-11 IPO price range)

- Market capitalization based on fully diluted shares outstanding

- “Blue Apron,” Wikipedia (https://en.wikipedia.org/wiki/Blue_Apron)

- Blue Apron Holdings Inc.’s SEC Form S-1/A Filing (June 19, 2017) (“APRN S-1”), at page 95

- Euromonitor APRN S-1, at page 113

- APRN S-1, at page 4

- Euromonitor, APRN S-1, at page 113

- APRN S-1, at page 106

- APRN S-1, at page F7. Free Cash Flow calculated as net cash flow from operations minus purchases of property and equipment and capitalized software development costs

- Source: Bloomberg, Company SEC filings and websites, Business Insider (http://www.businessinsider.com/amazon-fulfillment-centers-logistics-manufacturing-jobs-us-chart-2017-1), Hitwise, a division of Connexity, March 8, 2017, Tampa Bay Times (http://www.tampabay.com/things-to-do/food/cooking/recipe-delivery-services-blue-apron-plated-and-hellofresh-are-they-worth-it/2222468), and HelloFresh financial statements (https://www.hellofreshgroup.com/investor-relations-1)

- APRN S-1, at page 106

- APRN S-1, at page 98

- APRN S-1, at page 104

- APRN S-1, at page 106

- Cost per Customer, or CPC, is calculated as cumulative marketing expenses for the years 2014, 2015, 2016 and the first quarter of 2017, divided by the total number of Customers acquired during such period. The Cumulative Net Revenue columns reflect cumulative net revenue per Customer from Customers acquired between 2014 and 2016. Each column reflects cumulative net revenue for the Customers in the applicable cohort divided by the total number of Customers in that cohort. The chart presents the average cumulative net revenue generated by all Customers included in the applicable cohorts, including from Customers that ordered only once and then ceased ordering as well as those Customers that continued to order from us and thus ordered multiple times. For a Customer to be included in the calculation for a particular column, the length of time that has elapsed since the Customer first purchased from us must be at least as long as the time period indicated for such column. Accordingly, the number of Customers included in the cumulative net revenue per Customer columns decreases as the time intervals increase. For example, the six-month column is calculated using the cumulative net revenue during the first six months following a Customer’s first purchase from all Customers who first purchased from us between January 1, 2014 and September 30, 2016 (i.e., Customers who first purchased at least six months prior to the end of the first quarter of 2017). Customers acquired after September 30, 2016 are not included in any Cumulative Net Revenue column calculations because their first purchase occurred less than six months before the end of the first quarter of 2017

- Our Free Cash Flow calculation uses a tax-effected EBIT and adds depreciation and amortization less changes in working capital and capex

- Crunchbase.com and Pitchbook.com

- Year ending 2016 SEC Form 10-K, at page F-16

- Year ending 2015 SEC Form 10-K, at page 86

- Year ending 2014 SEC Form 10-K, at page 43 and Wikipedia (https://en.wikipedia.org/wiki/Grubhub)